IRS Form 3520: Why You Must Report Foreign Gifts of More Than $100,000

If you receive a large gift or inheritance from someone outside the United States, you may be required to report it to the IRS.

Many U.S. taxpayers are surprised to learn that foreign gifts or inheritances can trigger a reporting requirement even though the gift itself is not taxable.

IRS Form 3520 is the form used to report certain foreign gifts, inheritances, and transactions involving foreign trusts. Failing to file the form when required can lead to substantial penalties, even when no tax is owed.

This article explains when Form 3520 must be filed, how the reporting process works, and what options may be available if the filing deadline has already passed.

Quick Overview of IRS Form 3520

IRS Form 3520 is used by U.S. taxpayers to report certain transactions involving foreign trusts and large gifts or inheritances from foreign individuals or entities.

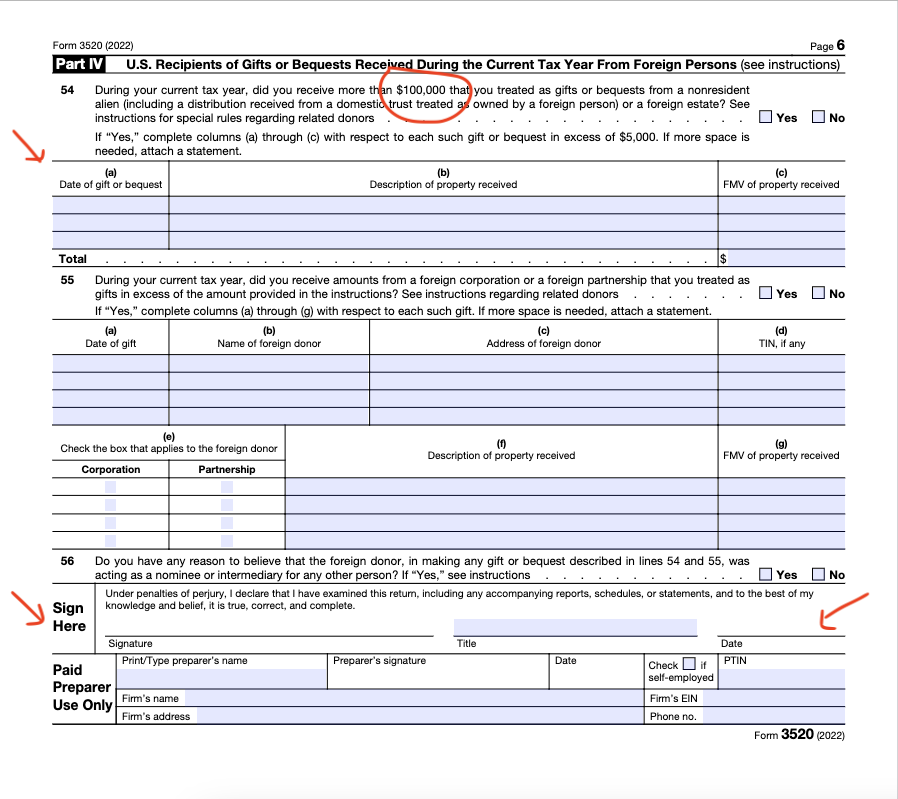

For many taxpayers, the most common reason to file Form 3520 is receiving a foreign gift or inheritance valued at more than $100,000 during a single calendar year.

Although foreign gifts of this type are generally not taxable, the IRS requires disclosure so it can track certain international financial transfers and ensure compliance with U.S. reporting laws.

Are Foreign Gifts or Inheritances Taxable in the United States?

Many taxpayers assume that receiving a large gift from overseas automatically creates a tax liability. In most cases, that is not correct.

Foreign gifts and inheritances received by U.S. taxpayers are generally not taxable income under U.S. tax law. However, even though the gift itself is not taxed, the IRS may still require the recipient to report the transfer.

This reporting requirement exists so the IRS can track large international financial transfers and ensure that income is not being disguised as a gift.

For that reason, U.S. taxpayers who receive foreign gifts or inheritances above certain thresholds must disclose the transfer using IRS Form 3520.

What Types of Foreign Gifts Must Be Reported?

The reporting requirement typically applies to large gifts or inheritances received from foreign individuals or foreign estates.

Examples of reportable gifts may include:

• Cash transfers from a foreign parent or relative

• Foreign investment accounts transferred as part of an inheritance

• Real estate or other property received from a foreign estate

• Financial assets transferred from a nonresident alien

In these situations, the value of the assets received during the year determines whether a Form 3520 filing is required.

Why the IRS Requires Foreign Gift Reporting

The purpose of Form 3520 reporting is not to tax the gift itself. Instead, the IRS uses the form to monitor certain cross-border financial transactions.

Without these reporting requirements, it would be difficult for the IRS to distinguish between legitimate gifts and transfers that might represent unreported income.

By requiring disclosure of large foreign gifts and inheritances, the IRS can verify that the transaction qualifies as a gift rather than taxable income.

Who Must File IRS Form 3520 for Foreign Gifts

A U.S. taxpayer may need to file Form 3520 when receiving large gifts or inheritances from foreign individuals or entities.

Common situations that trigger a filing requirement include:

- Receiving cash, financial assets, or property worth more than $100,000 from a nonresident alien in a single calendar year

- Receiving cash, financial assets, or real estate worth more than $100,000 from a foreign estate after the death of a foreign individual

The $100,000 threshold applies to the total amount received during the year from foreign individuals or estates.

It is also important to understand that Form 3520 may be required for smaller amounts received from foreign corporations or partnerships. In those cases, the reporting threshold is significantly lower and is adjusted periodically for inflation.

Form 3520 is also used for certain foreign trust transactions, though those reporting requirements involve additional rules beyond the scope of this article.

How to Report a Foreign Gift or Inheritance on Form 3520

IRS Form 3520 must be completed carefully because errors or omissions can lead to penalties.

The general reporting process typically includes the following steps:

- Confirm that you are a U.S. person who received a reportable gift or inheritance from a foreign individual or entity

- Complete the identifying information required on the form

- Report the value and description of the foreign gift or inheritance received

- Provide the date the gift or bequest was received and the fair market value of the assets

Foreign gifts are typically reported in Part IV of Form 3520.

{kind=link}

Because the form is used for several types of international reporting, taxpayers often consult a tax professional or tax attorney when preparing the form to ensure that the correct sections are completed.

When Is IRS Form 3520 Due?

IRS Form 3520 is generally due on the same date as the taxpayer’s federal income tax return.

For most taxpayers, the filing deadline is April 15 of the year following the year in which the foreign gift or inheritance was received. If the taxpayer files an extension for the income tax return, the Form 3520 deadline typically extends to October 15.

Unlike many tax forms, Form 3520 cannot be electronically filed.

The form must be mailed to the IRS service center that handles international tax filings in Ogden, Utah.

Internal Revenue Service Center

P.O. Box 409101

Ogden, UT 84409

If the form is filed accurately and on time, the IRS generally has three years from the filing date to examine the filing.

If the form is not filed when required, the statute of limitations may remain open indefinitely until the form is submitted.

What Happens If You Fail to File Form 3520?

Failing to file Form 3520 when required can lead to substantial penalties.

The penalty for failing to report a foreign gift or inheritance is generally 5 percent of the value of the unreported gift for each month the form is late. The maximum penalty can reach 25 percent of the value of the gift.

Because these penalties are based on the value of the gift or inheritance rather than unpaid tax, they can become extremely large even when no tax is owed.

If a taxpayer discovers the issue before the IRS initiates contact, it may be possible to file the form late and submit an explanation describing the circumstances that led to the missed filing.

Addressing Form 3520 Penalties

Taxpayers who receive a penalty notice related to Form 3520 may have an opportunity to challenge the penalty.

In many cases, the key issue becomes whether the failure to file was due to reasonable cause rather than willful neglect.

A reasonable cause argument typically requires demonstrating that the taxpayer acted responsibly and took reasonable steps to comply with the law once they became aware of the reporting requirement.

Supporting documentation may include records showing that the taxpayer sought professional advice, attempted to understand the filing requirements, or acted promptly once the issue was discovered.

Because the appeals process can be complex and time-sensitive, taxpayers often seek legal guidance when responding to a Form 3520 penalty notice.

Working With a Tax Attorney on Form 3520 Issues

Foreign gift reporting rules can be confusing, particularly for taxpayers who are unfamiliar with international tax compliance requirements.

Tax Attorney Sammy Kim has successfully convinced the IRS to eliminate massive Form 3520 failure-to-file and late penalties for her clients, including the removal of a penalty that was nearly $400,000.

Tax Attorney Sammy Kim focuses her practice on tax controversy and international tax reporting matters, including cases involving foreign gifts, inheritances, and Form 3520 penalties.

Her Fairfax, Virginia–based practice works with clients across the United States, and many matters can be handled through secure virtual appointments.

Taxpayers who discover that a foreign gift or inheritance may not have been reported correctly often seek legal guidance before contacting the IRS to better understand their options.

Schedule a consultation now to discuss your situation.

On Behalf of the Law Offices of Sammy Kim

IRS and State Tax Lawyer

The Law Offices of Sammy Kim helps clients handle tax issues with the federal or state tax authorities, including negotiating offers in compromise and installment agreements, reducing or eliminating tax debt, releasing wage levies, business bank levies, and tax liens, and relieving tax penalties for failure to pay.

Your IRS Tax Problem Has a Solution

That’s Right For You

More Tax Lawyer Tips

Owe The IRS After A Scam? Here’s What You Can Do About It

By On Behalf of the Law Offices of Sammy Kim |